Article

What goes on behind the scenes when an international payment is made? We reveal all and demonstrate the various processing stages.

Better understanding results in fewer errors. Here you will find an animated film explaining the basics of international payments.

Let's look at the four steps in the processing of an international payment

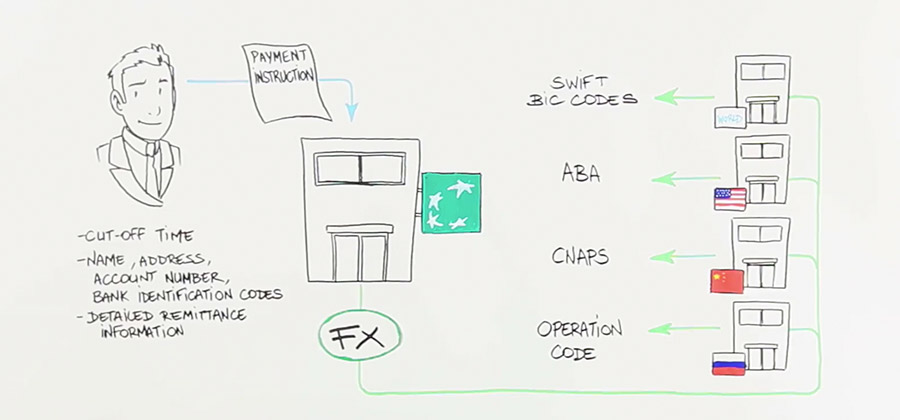

1. The customer sends the payment order to the bank

The payment order is sent to the bank via an online banking system (e-banking) or a bulk upload system, in other words a file containing a large number of payments.

- Banks have their own internal e-banking systems (such as Easy Banking Business at BNP Paribas Fortis), but there are also systems that can communicate with multiple banks, such as SWIFTNet and Isabel.

- A limited number of corporates and public institutions can send large volumes of payments to the bank directly from their own ERP systems via bulk upload (sometimes referred to as 'host-to-host').

Remember to provide all the necessary information in the payment request. For transactions outside the SEPA zone, specific rules often apply. A few typical examples:

Not sure what you're doing? Check the Currency Guide here for information on all currencies.

2. The bank validates the input and sets the payment in motion

The bank performs the necessary compliance checks. The bank has an obligation to carry out a number of checks, for example in order to prevent payments being sent to countries under embargo or to people/entities subject to financial sanctions. The EU, the US, the UN and individual countries have such embargo lists.

3. The bank chooses the appropriate routing for executing the payment

For payments in EUR in the SEPA zone, agreed clearing systems are used. Elsewhere in the world, there is no system that is able to connect with any bank in any currency. That makes things complicated, as your banker must find correspondent bankers to ensure the money is received by the final beneficiary. Banks usually have one or several correspondents in each country for the currencies they allow payments in. Matching them with one another for every payment is no small feat. When that has been done, the money can subsequently pass through each of those banks. Your bank will determine the optimal routing on the basis of a number of criteria. These are the main ones:

- 'In-house'

For payments between accounts held with the same bank. This is an accounting movement, whereby the money does not leave the bank. - 'Clearing

The daily transaction volumes between banks are enormous. They are processed in clearing systems. These systems process payments on a 'net basis': all incoming and outgoing payments are listed per bank, and then the net amount to be paid or received ('settled') is calculated for each bank in question. This process takes place multiple times a day. This is called 'net settlement'. Depending on the clearing system, there is usually a focus on either large, relatively urgent amounts or greater numbers of smaller, less urgent transactions. - ‘Correspondent banking’

The actual settlement can only take place in the country to which the currency belongs, i.e. via a local clearing system. Often, one of the two banks involved is not connected to the clearing system of the third country. In this case, direct routing to this system is not possible.

The solution? A 'correspondent bank' that does have access to the local clearing system. Many banks have a worldwide network of such correspondent banks. They hold accounts with them (called 'nostro' accounts) via which they can route payments. The correspondent bankers then settle the amounts so that the beneficiary bank receives the money and can pay the final beneficiary.

4. The customer receives the details of the payment

The entire process concludes with reporting: the customer sees all credit and debit information on their bank statements.

Watch out for 'restricted' currencies

Only convertible currencies can be used to make international payments. Some currencies are 'restricted': this means that in accordance with local legislation, these currencies are not permitted to leave the country. As such, it is not possible to open an account in Belgium in this currency or to use it to make international payments.

An example of a 'restricted' currency is the BRL, the Brazilian real. Banks have a workaround for this problem. They conclude an agreement with a correspondent who does have access to the currency. They send the equivalent value in EUR or USD, convert the amount into the local currency in the country (in this case BRL), and forward that amount to the beneficiary.

What is SWIFT?

To ensure routing is successful, banks communicate with one another via the SWIFT network (Society for Worldwide Financial Communication). SWIFT is owned by financial organisations worldwide. There is a specific standard for each form of communication, for example MT 101, MT 202, etc. In the case of SWIFT, a specific address is also required: the BIC (Bank Identification Code).

Article

07.11.2024

BNP Paribas Fortis Factor: the oxygen to your growth story

Factoring is playing an increasingly important role in promoting the growth of Belgian and international companies. BNP Paribas Fortis Factor provides the oxygen to their growth story.

You want your business to grow and thrive, and so all the help and guidance you can get are more than welcome. The reason is clear: support brings extra energy to your entrepreneurial spirit and essential resources to fuel your innovative growth plans.

BNP Paribas Fortis Factor, a subsidiary of BNP Paribas Fortis, offers a service designed precisely for that: to relieve stress and motivate, to promote and nurture your growth. In this interview, Jef Ramaekers, Head Factoring Benelux at BNP Paribas Fortis Factor, and Audrey Bourguet, Working Capital Advisor at BNP Paribas Fortis Corporate Banking, come together to discuss one key topic: Factoring and the positive role it can play for Belgian businesses and their international branches.

Explaining factoring succinctly, however, is a challenge. Jef Ramaekers, Head Factoring Benelux at BNP Paribas Fortis Factor, clarifies: “To start with, factoring is a means, not an end. It’s a tool for business owners or CFOs to optimise working capital. Every financial manager, in any company, will at some point ask the same question: ‘Who do I need to pay, when, and how can I pay them with the resources I have?’ Simply put, factoring enables businesses to pay suppliers without waiting for customer payments to come in. We finance invoices by converting them into directly available cash for the business.”

This process actively alleviates concerns and reduces stress factors, allowing entrepreneurs to focus on what they do best – running their business. Ramaekers adds, “We like to say ‘giving oxygen to growth stories.’ But I certainly see the value in the term ‘relieving stress’ here. By giving an entrepreneur or CFO the freedom to focus on core activities and by taking on a key part of the financial management, we create extra time and opportunities. And they also have less to worry about."

Positive shift

According to Ramaekers, the traditionally negative perception of factoring is a thing of the past: “Factoring was once seen by many business leaders as a ‘lender of last-resort’ – a way to borrow money from the bank by using assets, receivables, or customer invoices. In other words, a company’s last resort. Fortunately, those days are long behind us. We’ve evolved towards a very open attitude to factoring, allowing our division to grow into a true service provider. Our clients’ primary need remains short-term financing. Today, one in five invoices in our country is paid through factoring. Factoring is now a substantial market, representing more than one hundred billion euros per year. BNP Paribas Fortis Factor manages 41 per cent of this market, accounting for EUR 55 billion at the end of 2023.

Growth

From the bank’s perspective, factoring also represents a significant growth story. Audrey Bourguet, Working Capital Advisor at Transaction Banking for BNP Paribas Fortis, explains: “Today, factoring is the financial product that nicely aligns with the rising turnover of our companies. It provides a practical solution for working capital and is part of a suite of Transaction Banking services. In addition to Factor, this also includes Global Trade Solutions, Cash Management, Fixed Income, and Working Capital Advisory. All these services share a common goal: provide the best possible solution for our clients’ financial needs and be there for them in all situations where they can benefit from our support.”

Factoring, from the bank’s standpoint, represents an increasingly strong and positive story, unlinked from its past connotations. Bourguet adds, “You can see this in how we truly integrate factoring within our bank and the group, and in how we offer this service to businesses across all sectors and sizes. We work with a wide range of companies in the Belgian economy. As a result, we have seen that it is precisely those companies that succeed in optimising the funding of their working capital by making use of our factoring services, among other things. This reinforces our belief that it is a very positive story: we’re talking about a form of financing that seamlessly adapts to the growth of any business, large or small.”

Natural evolution

Factoring is available to small, medium-sized, and large companies alike. Ramaekers says, “We aim to provide a solution that supports businesses throughout their entire lifecycle – we’re genuinely unique in the market in this regard. This means that we are there for start-ups, SMEs, multinationals, and every type of business in between. We are the only bank on the market to have a digital solution for small businesses in the form of Easy2Cash. This digitalisation makes it a very cost-effective option with highly competitive margins, but also a reliable, particularly fast and up-to-date link with our customers and their accounting, using a digital yet personal approach. Although Easy2Cash is digital, it includes a dedicated contact person, making the solution both personal and accessible. For start-ups, for example, it’s often challenging to secure credit. For these modest, short-term credit needs, we provide a solution in consultation with the BNP Paribas Fortis banker, enabling them to keep growing without being hindered by their expanding requirements for financing, automation, accounting, etc. Factoring gives them additional resources to meet these needs.”

Ramaekers notes that the steady growth of young companies also demands an adaptation of financial services: “It’s a natural evolution that benefits both partners. If your business grows, we grow with you – it’s that simple. During all those specific growth moments – when entrepreneurs start considering additional staff or potential exports – factoring grows with them. And we do this together with the bank; the group behind this story plays as a team. And let’s not forget, we’re here even if more challenging times come. We’re well aware that a company’s journey is not always easy. It’s at those moments that the value of our expertise and the support we provide really stands out.”

When a company grows into a large enterprise with the profile of a multinational, the importance of factoring further increases. Ramaekers says, "More than 65% of the really large companies in Belgium, with a turnover of more than EUR 1 billion, use factoring services. And half of them are our customers. Factoring often provides additional economies of scale for large enterprises. For example, we can finance receivables that have no impact on a company’s debt ratio. By combining invoice pre-financing with credit insurance, companies can avoid having debt on their balance sheet, with the approval of the company auditor. It’s a technical matter, but it is this combination of various financial elements that makes factoring efficient, high-performing and valuable for many companies.”

Economic fabric

The two agree on the value of factoring in supporting the economic fabric. Bourguet explains, “Part of this supportive role is due to the fact that factoring is a completely transparent financial service – you can only finance what is effectively there.” Ramaekers adds, “Absolutely. Plus, factoring sits right in the middle of the value chain, embedded in the economic fabric. We work alongside our clients, their customers (debtors), the bank, and so on. This makes us a key figure in this chain. We coordinate and facilitate. And for this we need to have our feet firmly planted on economic ground, often for the benefit of all our customers. When we succeed in, for example, reducing the payment terms of invoices for a business, it has a positive ripple effect not only for that company but for the economic process as a whole. This is why I am convinced that we play a broad role in the economic ecosystem – often broader than is generally perceived.”

Opportunities and fair guidance are also crucial in this financial field. Ramaekers says, “At Factor, we engage in transparent discussions with the bank and our clients to find the best solution for their needs. This means we identify opportunities and often suggest them, but also act as an honest, proactive sounding board. It’s about dialogue, analysis, and constructive critique.” Bourguet concurs: “I completely agree. With a service like factoring, we are deeply involved in our clients’ economic activity – the entrepreneurs who rely on us. So, we take a broad view of every case, looking beyond just a banking product or a single solution. This is what makes BNP Paribas Fortis’s approach so strong: we operate as a team, consisting of specialists from both Factor and the bank. This group of experts from different, well-coordinated entities provides entrepreneurs and companies with a comprehensive approach, even for complex cases. These are the moments when we truly rely on our internal expertise: years of experience; colleagues with solid knowledge; reliable economic data applicable to numerous scenarios. This combination enables us not only to guide companies in the right direction but also to provide financial support that is fair, safe, and sound.”

Future

Just like the bank itself, BNP Paribas Fortis Factor frequently considers its strategic direction for the future. As a provider of forward-thinking services, it’s essential to adopt a future-oriented approach to financial services. Ramaekers notes, “Earlier, I mentioned our digital solution, Easy2Cash. I think we can be quite proud of this because it is a glimpse into the future – today. Beyond that, our services are evolving very organically towards the future: we’re constantly striving to make them accessible to an ever-wider group of clients across the economic landscape. Additionally, we’re very focused on sustainability.”

Bourguet adds, “This last aspect is a natural extension of what we do at the bank every day. Our commitment to sustainability extends seamlessly to factoring: we encourage and motivate our clients to join us on this sustainable path.”

The two teams also collaborate closely in developing new services. Ramaekers explains, “We see a significant evolution in the commercial sector, with many online stores offering deferred payment options, such as a 30-day extension. This practice is also increasingly common in the B2B market. Factoring can innovate in this area, so we see it as part of the future we’re actively developing. From a European perspective, there are other innovations too: e-invoicing, for example, is soon to become the standard for all businesses. This presents both a challenge and an opportunity in terms of services and advisory, which we’re shaping together with the bank.”

The two partners have also developed new services. Ramaekers: "We have observed a remarkable evolution in the commercial sector, where many online stores offer payment delays of 30 days, for example. This practice is also increasingly common in the B2B market. Factoring can offer an innovative solution, so this is part of the future that we are currently developing. On the European level, there are also new features: e-invoicing will soon become the norm for all companies. This presents both a challenge and an opportunity in terms of services and advice, which we are developing together with the bank."

Bourguet concludes, “It’s clear that this is a story of synergy, one where we work together seamlessly. This isn’t just rewarding for us but also for our clients. We’re rooted in the heart of the economic marketplace, yet we’re also focused on creating platforms and products that will lead the way and shape the future of this market.”

More information: https://factor.bnpparibasfortis.be/

Article

10.06.2024

Electronic invoicing between companies to become mandatory

The bill to introduce this obligation in Belgium has been submitted to the Federal Parliament. If the draft bill is approved, B2B e-invoicing will become mandatory from 1 January 2026. Our experts explain why Belgium wants to introduce these new rules, what the implications are for your company and how we can better support you.

“The bill is consistent with international developments and initiatives at the European level,” says Nicolas De Vijlder, Head of Beyond Banking at BNP Paribas Fortis. "Europe's ambition is a harmonised digital standard. Structured e-invoicing between companies will also reduce the administrative burden of invoicing, enabling companies to work more efficiently and increase their competitiveness. The automation of VAT declarations will also help governments prevent tax fraud and adjust economic policies based on more qualitative data.”

Evolution rather than a revolution

“The new legislation is an evolution rather than a revolution,” adds Erik Breugelmans, Deputy Managing Director at BNP Paribas Factoring Northern Europe. "Digitalisation is becoming pervasive at all levels of society, as we have seen with the increase in electronic payments, as well as the additional obligations in recent years regarding electronic invoicing to the government. In this sense, the bill for mandatory electronic invoicing between companies is a logical next step. Our bank is happy to contribute to this process, although we do not intend to offer the same services as accounting software or fintechs. However, we are happy to help our customers with payments and financing."

The impact on businesses

“Customers need to be aware that the new regulations will have an impact on their internal and external processes,” continues Erik Breugelmans. "The majority of Belgian companies mainly serve an international market, which means that the introduction of electronic invoicing will be more complex for them than for companies operating in the domestic market. As the legislation will be introduced in one go, they need to start preparing now."

“The new rules will affect a company’s accounting department as well as its IT department,” emphasises Nicolas De Vijlder. "The procedural requirements are key, otherwise the automated process will not work. However, one of the main benefits of advanced automation is that everything can be done faster and more efficiently. The time between sending an invoice and paying it will be shorter and cash flows more predictable. In addition, it will also reduce the risk of error and fraud, as all transactions will pass through a secure channel."

Ready to offer you even more and better support

“Thanks to the far-reaching digitisation resulting from the new regulations, we will be able to further optimise payments,” concludes Erik Breugelmans. "As a bank, we need to finance our customers’ receivables as quickly and efficiently as possible, so that they have easier access to their working capital. In addition, because we have already gone through an entire process in terms of large-scale automation, we will be able to adapt quickly to the new rules. We can also draw on the expertise of the BNP Paribas Group, which is currently developing an e-invoicing solution for large companies."

Want to know more?

Listen to the episode on B2B e-invoicing :

Article

31.05.2021

Optimise your working capital with factoring

How can you keep your working capital healthy while incorporating the requisite financial flexibility? Factoring helps you to finance your cash requirements in a proper, timely and suitable way.

Securing liquidity is the key to financing your working capital requirements and keeping your business running smoothly at all times. That's exactly what factoring offers.It is a structural solution for optimising working capital. In the video below (in Dutch) in less than half an hour you will gain a clear picture of what factoring has to offer.

If you prefer to watch the video in French, click here.

Factoring: a tailored structural solution

In exchange for transferring your invoices to an external factoring company, you can count on fast, flexible financing, monitor the collection of your invoices, and protect yourself against potential bankruptcy among your customers. Each factoring solution is tailored to fit the needs of your business. This includes companies operating at international level. In Belgium, one in six companies currently outsource their invoices to an external factoring company. The same trend is evident in other European countries.

Do you have any questions, or would you like to discuss how factoring can help you? Contact your relationship manager or send us your details via the contact form and we will get in touch with you.

Article

26.10.2018

How to automatically get the best exchange rate

Companies working with several currencies often want to avoid exchange rate risks and administrative hassle. That is why the bank has come up with a behind-the-scenes solution: the 'embedded FX' service.

Embedded FX? You don't even need to remember the name, because the system works automatically, without you even having to think about it. FX doesn't stand for Hollywood-style special effects, but for Foreign Exchange, sometimes referred to as Cross Currency. You are guaranteed to come across this at some point if you make international payments, since they are not always executed in the currency of the debit account (referred to as 'mono-currency payments'). Sometimes, the currencies of the accounts the payment is being debited from or credited to may not be the same. These are FX payments. During such payments, an exchange takes place: one currency is sold and another bought, without you having to lift a finger.

The volumes on the FX market might be greater than you'd think. To put it plainly: they are enormous. Every day, more than 5 trillion American dollars are traded. That is 5000 billion American dollars, more than the volume involved in global equities trading...in a single day. The FX market operates day and night, and only closes over the weekend from 10 pm on Friday until 10 pm on Sunday.

Wim Grosemans (Head of Product Management Payments and Receivables at the BNP Paribas Cash Management Competence Center):

'On the FX market, banks essentially play the role of a wholesaler: they buy and sell currencies on the international market, and then sell them on to the customer with a mark-up. BNP Paribas is one of the biggest players, ranking among the global top ten. There is no official market rate in this over-the-counter market. Each bank determines the rate at which it wants to buy and sell currencies itself. Unofficial market rates can be found in publications from a number of public institutions (such as the European Central Bank) and private organisations (Reuters, Bloomberg etc.). These are based on the average rate offered by a number of major banks.'

The rate is always determined per currency pair, for example the euro versus the American dollar: EUR/USD = 1.1119. The most traded pair is EUR/USD, which represents 25% of daily trade. Second on the list is the pair American dollar/Japanese yen

(USD/JPY) with 18%, with British pound/American dollar (GBP/USD) coming in third at 9%.

Alwin Vande Loock (Product Marketing Manager Payments and Receivables at the BNP Paribas Cash Management Competence Center):

'As for the rate, banks offer a number of options. The rate can be a live market rate that is continuously being updated. The EUR/USD rate, for example, is adjusted more than 50 times per second. Another option is a daily rate. In this case, a rate is offered that will apply for a certain period.'

For many companies, all of this hassle with exchange rates is a real headache. Too complex, too expensive in terms of administrative costs and too many exchange rate risks. For those customers, banks have a solution: embedded FX.

Wim Grosemans (Head of Product Management Payments and Receivables at the BNP Paribas Cash Management Competence Center):

'When you make a payment in a currency you do not hold an account in, the bank will immediately retrieve a good exchange rate from its colleagues in the dealing room of the Global Markets department. The rate is usually confirmed within one hour after the customer has sent the payment. Unless large amounts are being transferred, the entire process is automatic. The IT systems used are much more efficient than they were just a few years ago, meaning that the bank is less exposed to volatility and can offer its customers a competitive rate. Embedded FX is an efficient and simple alternative for anyone who doesn't want to hold accounts in different currencies and run the exchange rate risks that entails. For the customer, it no longer matters what currency they use: the process is exactly the same. What's more, it gives them peace of mind, because they know that they'll always get a great rate.'